Quantile combination: An application to US GDP growth forecasts

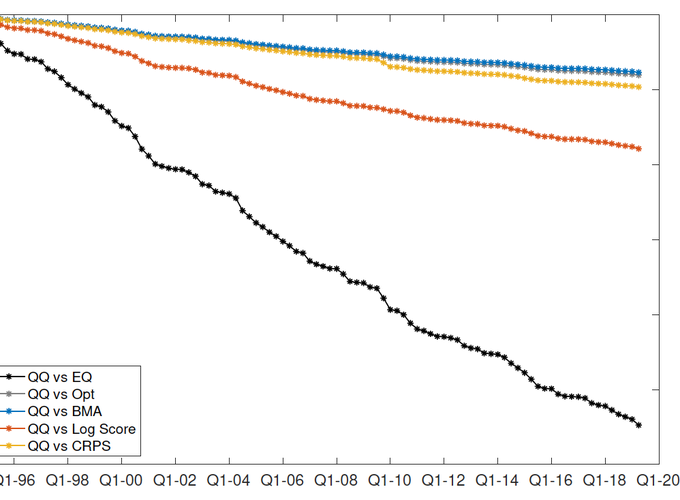

Cumulative CRPS for alternative approaches to forecast and combination for one-year ahead US GDP growth forecasts.

Cumulative CRPS for alternative approaches to forecast and combination for one-year ahead US GDP growth forecasts.

Quantile combination: An application to US GDP growth forecasts

Abstract

We propose an easy-to-implement framework for combining quantile forecasts, applied to forecasting GDP growth. Using quantile regressions, our combination scheme assigns weights to individual forecasts from different indicators based on quantile scores. Previous studies suggest distributional variation in forecasting performance of leading indicators: some indicators predict the mean well, while others excel at predicting the tails. Our approach leverages this by assigning different combination weights to various quantiles of the predictive distribution. In an empirical application to forecast US GDP growth using common predictors, forecasts from our quantile combination outperform those from commonly used combination approaches, especially for the tails.